Shipping Fuel Shock & Margin Math: How Rising Port Costs Are Reshaping Dropshipping Economics in 2026

Maersk disclosed $500 million per month in additional fuel costs on May 7, 2026, driven by the closure of the Strait of Hormuz and the resulting scramble for bunker fuel outside the Persian Gulf.

Shipping Fuel Shock & Margin Math: How Rising Port Costs Are Reshaping Dropshipping Economics in 2026

Maersk disclosed $500 million per month in additional fuel costs on May 7, 2026, driven by the closure of the Strait of Hormuz and the resulting scramble for bunker fuel outside the Persian Gulf. That figure, reported by The Loadstar, represents what a single ocean carrier is absorbing before any of that cost reaches your shipping label. Hapag-Lloyd put its own increase at $50 million per week. These aren't projections or scenario models. They're current burn rates, and every dollar is working its way downstream toward the parcel surcharges that determine whether your store's margins survive the summer.

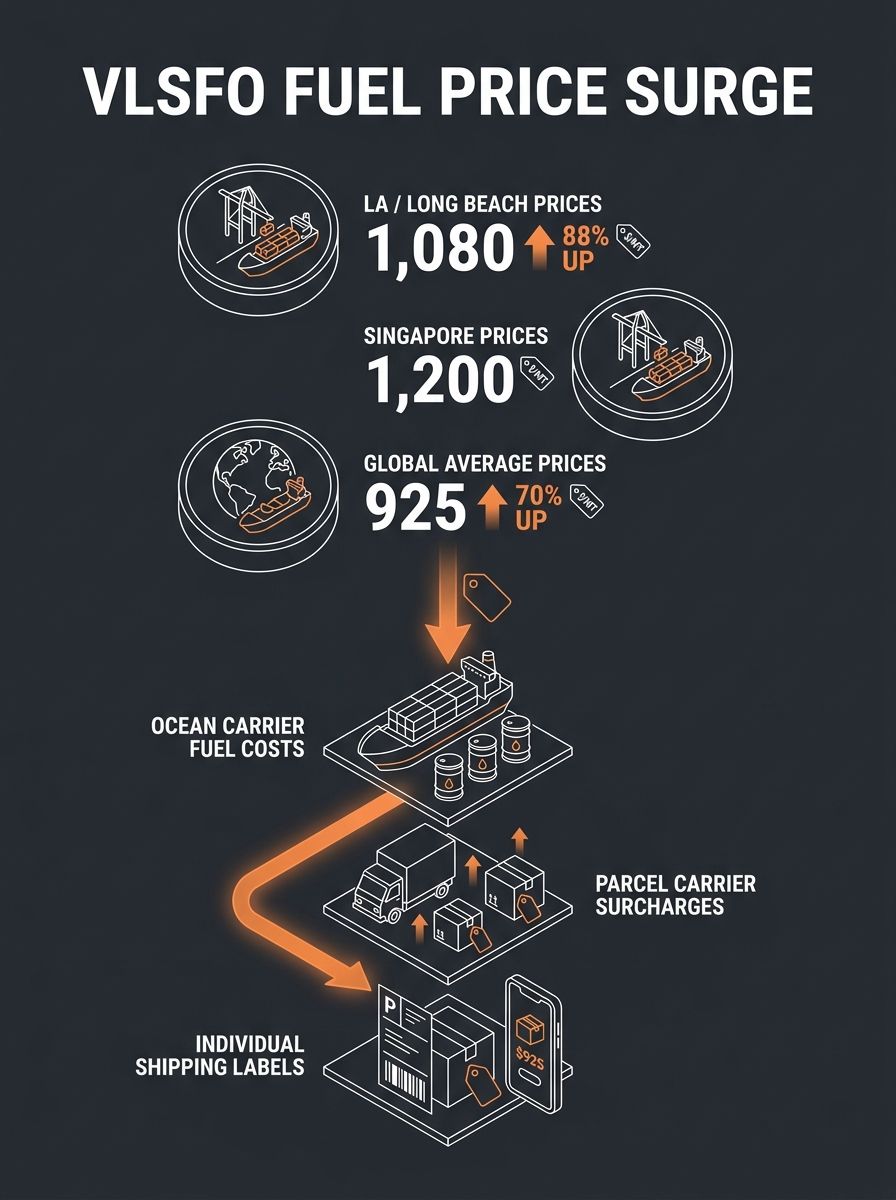

The average price of very low-sulfur fuel oil (VLSFO) has climbed 70% globally to $925 per metric ton since the conflict began. At the Ports of Los Angeles and Long Beach, where a huge share of Asia-sourced consumer goods enters the U.S., that number is $1,080 per metric ton, an 88% increase. Singapore, the world's largest bunkering hub, has seen VLSFO exceed $1,200 per tonne, with low-sulfur marine gas oil surpassing $2,000. If you're dropshipping products that travel through any of these nodes, your cost basis shifted weeks ago whether you noticed it or not.

Every Carrier Has Moved. Here's the Damage.

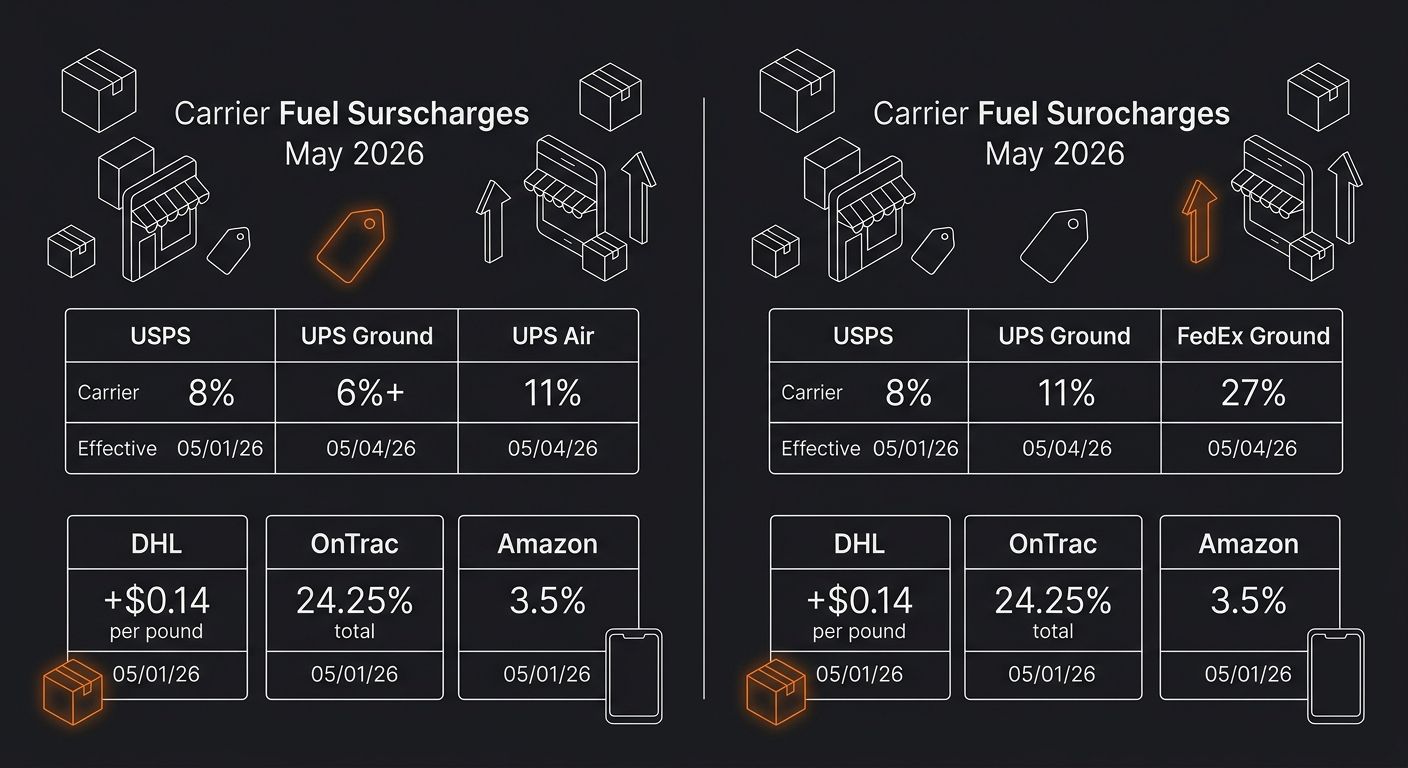

The fuel surcharge impact has hit every major carrier within a compressed window. USPS launched its first-ever fuel-related fee on April 26, 2026, an 8% increase on Priority Mail, Priority Mail Express, and Ground Advantage labels that runs through at least January 16, 2027. That's nine months of guaranteed higher costs on what many dropshippers treat as their budget-friendly domestic option. UPS raised its domestic ground fuel surcharge by over 6% and air services by 11%, and critically, it raised the floor on its fuel surcharge table, meaning even if diesel prices drop tomorrow, you'll still pay more than you did in January. FedEx applied a 27% fuel surcharge on ground services for the week of April 20, nearly matching UPS's 27.50%.

And the less obvious players followed suit. DHL eCommerce is raising its domestic fuel surcharge by $0.14 per pound across all existing fuel price tiers effective May 30, 2026. OnTrac bumped its surcharge by 1.5% on April 6, bringing the total to 24.25%. Amazon introduced a 3.5% fuel and logistics surcharge in April with no end date specified. UPS also quietly rolled out a $5.00 Non-Compliant Label Fee for Ground Saver shipments effective May 4, adding operational cost for anyone whose labeling doesn't meet new requirements.

The pattern is clear: shipping cost inflation isn't arriving as a single rate hike you can absorb and forget. It's a stacking effect where base rates, fuel surcharges, and new compliance fees compound on every label. If you're shipping 500 orders a month through USPS Priority Mail at an average package weight of 1.2 lbs, that 8% surcharge alone adds roughly $0.60–$0.90 per label depending on zone. That's $300–$450 per month in new costs before you account for any base rate changes. Scale that to 2,000 orders and you're looking at $1,200–$1,800 per month in margin erosion from a single carrier's single surcharge.

The Unit Economics Problem Nobody's Pricing For

Here's where the dropshipping profitability crisis gets concrete. Take a product with a $29.99 retail price, a $9 landed cost from your supplier (product plus their fulfillment fee), and a $6.50 domestic shipping cost pre-surcharge. Your old contribution margin looked like this: $29.99 minus $9.00 minus $6.50 minus roughly $1.20 in payment processing (4% of sale price), leaving you $13.29 before ad spend. If your target customer acquisition cost was $10, you were clearing $3.29 per order. Thin but workable at volume.

Now run the same math with current surcharges. That $6.50 shipping cost picks up the USPS 8% fuel fee plus base rate adjustments from January, pushing it to roughly $7.40–$7.80 depending on your zone mix. If you're using UPS or FedEx instead, the jump is steeper. Your contribution margin drops to $11.99–$12.39, and with the same $10 CAC, you're clearing $1.99–$2.39 per order. That's a 28–39% drop in per-order profit. For operators already running at tight margins, that's the difference between a viable business and one that bleeds cash every month it scales. This is the margin erosion supply chain dynamics create when you can't pass costs through fast enough.

The instinct is to raise prices, but the math on that deserves scrutiny too. Bumping from $29.99 to $32.99 recovers most of the margin loss, but conversion rate sensitivity at the $30 price threshold is real. If your conversion drops even 8–10% from the price increase, your total profit per hundred visitors may actually decrease despite the higher per-order margin. This is why understanding contribution margin at the product level matters more than ever. Two products generating the same revenue can produce wildly different profits, and the gap widens as shipping costs increase because heavier or bulkier items absorb more of the surcharge.

The suppliers themselves are adjusting too. As a recent analysis of retail freight cost pressures noted, teams are switching suppliers, reducing timing buffers, and absorbing higher freight costs to maintain feature support and pricing. Dropshippers downstream of those decisions inherit the consequences: longer lead times, less predictable inventory, and occasionally degraded product quality as suppliers cut corners to hold their own margins. If you haven't revisited your supplier vetting process since the surcharges kicked in, your landed cost assumptions are probably stale.

So what does an operator actually do with this information? The first move is mechanical: pull your real shipping cost data from the past 30 days, not the rates you quoted yourself three months ago, and run your contribution margin at the SKU level. Kill or reprice anything where the updated shipping cost pushes per-order profit below your CAC. The second move is structural: evaluate whether sourcing directly from suppliers rather than through platform aggregators gives you enough per-unit savings to offset the surcharge increases. A $3–$5 reduction in product cost can completely neutralize the fuel surcharge impact on a mid-priced item. The third move is geographic: if you're still shipping everything from China through transpacific routes, your exposure to this specific disruption is maximum. U.S.-based and India-based suppliers remove the ocean freight variable entirely for domestic orders, even if per-unit costs run slightly higher.

The Uncomfortable Timeline

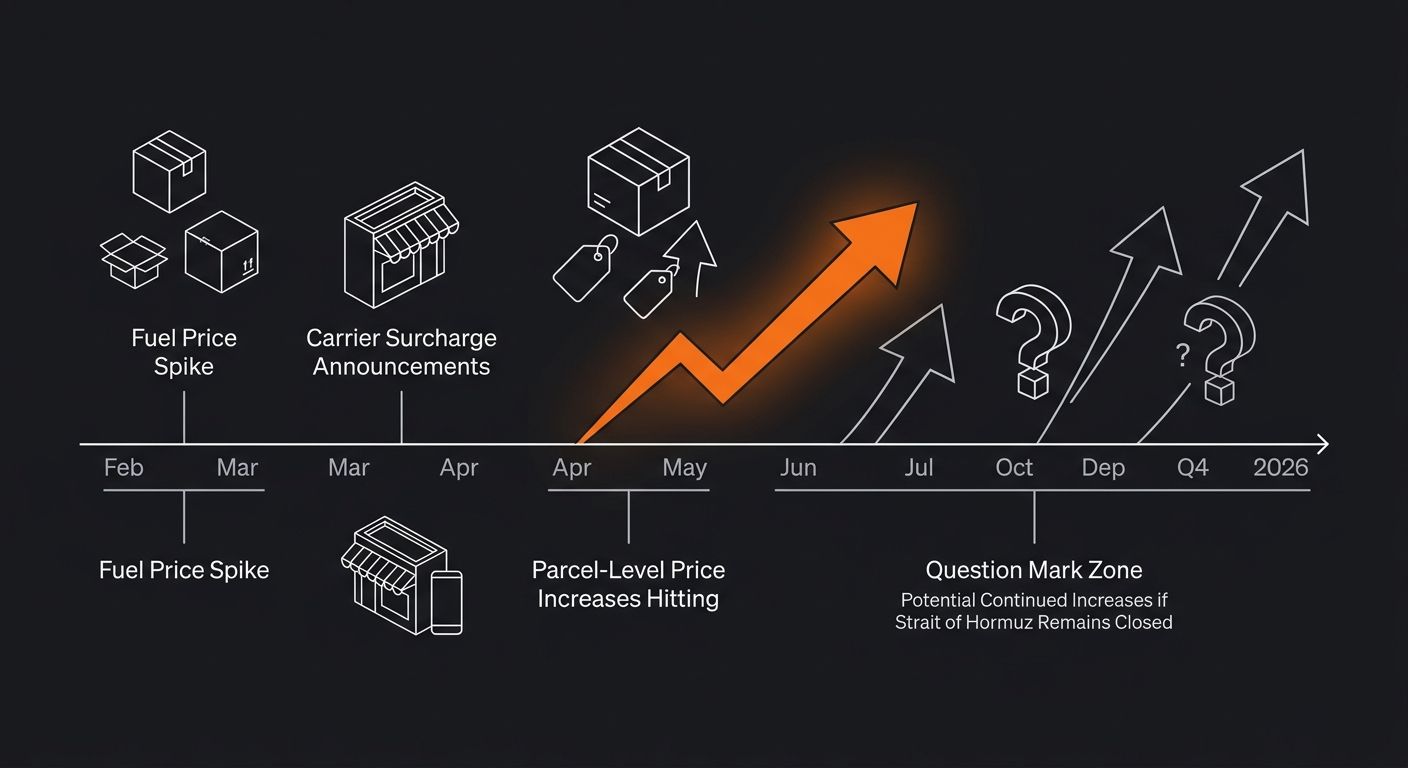

The question hanging over all of this is duration. If the Strait of Hormuz reopens in weeks, fuel prices will begin to normalize, though the "rocket-and-feather" dynamic in fuel pricing means surcharges will come down slower than they went up. Carriers have every incentive to maintain elevated surcharges as long as the market tolerates them. UPS raising the floor on its fuel surcharge table is a structural change, not a temporary one. USPS setting its surcharge window through January 2027 is a signal about expectations, not a worst-case hedge.

But if the disruption extends through summer and into Q4 — peak season for e-commerce — the compounding effects become severe. Carriers that are currently slow-steaming to conserve fuel will face pressure to speed up for holiday delivery windows, burning more expensive fuel at exactly the wrong time. Container vessel average speed has already dropped 2.3% since late 2025, falling from 15.58 to 15.18 knots, the lowest since March 2023. On North–South trade routes, speed reductions hit 3.6%. Slower ships mean longer transit times, more inventory tied up in transit, more stockouts, and more of the post-order cost problems that quietly eat profit after the sale. The hidden cost layer that tariffs and duties add to cross-border shipments will stack on top of elevated fuel surcharges, creating a landed cost environment where products that were profitable at $29.99 in January need to sell at $37–$39 to maintain the same margin.

The 2022 energy shock from the Ukraine conflict provides a useful baseline. During that episode, e-commerce sales growth dropped from 25.7% to 6.5%, and inflation-driven cost increases persisted for 18 or more months. The current disruption has a different character because the Strait of Hormuz carries roughly 20% of global oil supply, and Reuters reported this week that inventories will continue falling even if the conflict ends because it will take weeks for shipments to resume and reach refiners. Port of Los Angeles Executive Director Gene Seroka stated on May 8 that fuel now accounts for approximately 25% of the total cost of a voyage from Asia to Los Angeles, up from closer to 15% eighteen months ago. Matson CEO Matt Cox warned the same day about a timing lag between incurring fuel costs and recovering them through surcharges, which means the surcharges you see today reflect fuel prices from weeks ago, and the ones arriving in June and July will reflect what's happening at the pump right now.

What I can say with confidence is that the dropshippers who survive this cycle will be the ones who treated their shipping cost line as a variable that updates weekly, not a fixed assumption baked into a pricing spreadsheet from Q1. The data is moving fast, the surcharges are stacking, and the geopolitical situation that caused all of this shows no signs of quick resolution. Pricing your products with stale shipping data right now is functionally equivalent to running your store at a planned loss and hoping volume makes up the difference. Volume never makes up the difference on negative-margin orders. It accelerates the loss.

365 Dropship Editorial

Editorial team writing about E-commerce, dropshipping, and product discovery — reviews of dropshipping suppliers and platforms, trending niche guides (jewelry, beauty, pets, home, fashion), supplier due diligence, ecom operations, shipping & fulfillment strategy, product research, AOV optimization, and profitable dropshipping case studies.

Related Articles

Bunker Fuel Shocks & Last-Mile Economics: Why Global Port Disruptions Are Reshaping Dropshipping Unit Economics in 2026

On February 28, 2026, the Strait of Hormuz closed to commercial shipping traffic as the Iran conflict escalated into a direct naval blockade. Over 90% of crude and refined product exports from the Persian Gulf were cut off within 72 hours.

Cross-Border Tariffs & Import Duties: The Hidden Margin Killer Dropshippers Overlook

Every package entering the U.S. from China now triggers a full customs entry.

Cuba, Tariffs & Your Supply Chain: How Geopolitical Shipping Suspensions Force Dropshippers to Rethink Supplier Diversification in 2026

Executive Order 14380, signed January 29, 2026, declared a national emergency over Cuba and introduced a tariff framework targeting any country that supplies oil to the island. For dropshippers, the fallout reaches far beyond Cuba.

Explore more topics